METAVERSE BANKING: YOUR FIRST MOVER ADVANTAGE

As money, payments, and digital assets continue to advance, banks and financial institutions are faced with a growing need to innovate their services and business models.

As of today, a significant number of banks and financial institutions have already transitioned to the Web3 world, while many others are considering the move. According to experts, those who succeed in the transition to Web 3.0 will be at the forefront of technological advances in the coming years.

When banks slowly made the transition to the Internet in the 1990s, banks, and financial institutions that refused to enter the Internet era at that time stalled growth while those that embraced technology grew rapidly.

As banks and financial institutions had to adapt to the Internet era in the 1990s, they must now prepare for Web 3.0. With Web3 technologies like the metaverse, blockchain, and decentralized finance (DeFi), the financial industry could undergo a transformation, offering new levels of security, transparency, and control to customers.

62% of Gen Z’s don’t have any bank accounts at all.

Gen Z and Millennials are similar in many ways, but what will likely distinguish them the most moving forward is the influence of the pandemic. Millennials lived their adulthood through the lens of the 2008 financial crisis, while for Gen Z the lens is Covid.

As of today, a significant number of banks and financial institutions have already transitioned to the Web3 world, while many others are considering the move. According to experts, those who succeed in the transition to Web 3.0 will be at the forefront of technological advances in the coming years.

When banks slowly made the transition to the Internet in the 1990s, banks, and financial institutions that refused to enter the Internet era at that time stalled growth while those that embraced technology grew rapidly.

As banks and financial institutions had to adapt to the Internet era in the 1990s, they must now prepare for Web 3.0. With Web3 technologies like the metaverse, blockchain, and decentralized finance (DeFi), the financial industry could undergo a transformation, offering new levels of security, transparency, and control to customers.

62% of Gen Z’s don’t have any bank accounts at all.

Gen Z and Millennials are similar in many ways, but what will likely distinguish them the most moving forward is the influence of the pandemic. Millennials lived their adulthood through the lens of the 2008 financial crisis, while for Gen Z the lens is Covid.

Figuring out what the next generation wants has been a million-dollar question.

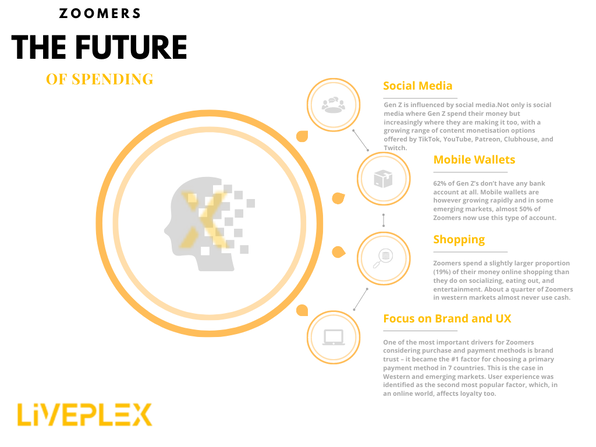

Nearly all Zoomers (GenZ) in the United States shop online, and because almost four out of five of them (78%) are TikTok users, over half (55%) say they have bought something they first saw on TikTok, and 65% say they get ideas of things to buy from all social media platforms.

Millennials and Gen Z are very brand loyal and appreciate a strong brand.

To achieve growth and success in 2030, businesses must start to understand the living, shopping, and financial habits of Gen Z or Zoomers (consumers aged between 16 and 24) now and accept that they are very different from previous generations. This demographic, which never knew life without the internet and smartphones, currently represents the largest population group on earth. Members of this age group account for almost 2.5 billion people, surpassing Millennials in 2019.

Nearly all Zoomers (GenZ) in the United States shop online, and because almost four out of five of them (78%) are TikTok users, over half (55%) say they have bought something they first saw on TikTok, and 65% say they get ideas of things to buy from all social media platforms.

Millennials and Gen Z are very brand loyal and appreciate a strong brand.

To achieve growth and success in 2030, businesses must start to understand the living, shopping, and financial habits of Gen Z or Zoomers (consumers aged between 16 and 24) now and accept that they are very different from previous generations. This demographic, which never knew life without the internet and smartphones, currently represents the largest population group on earth. Members of this age group account for almost 2.5 billion people, surpassing Millennials in 2019.

Customers are demanding new banking experiences that go beyond traditional financial services with the rise of Web 3. The Web 3 revolution requires banks and financial institutions to embrace the technology and infrastructure necessary to satisfy these new customers. Financial landscapes are rapidly evolving, and those who fail to adapt risk being left behind.

Over the last decade, fintech, or financial technology, has become one of the hottest high-growth sectors as businesses embrace the idea of improving banking and other financial services by leveraging technologies and implementing a client-centric approach. This fascinating concept has revolutionized how people access financial services, which are now faster and more convenient than ever.

From online banking to peer-to-peer lending, the fintech industry has seen rapid expansion and innovation. These advances have made it easier for individuals and businesses to access financial services, creating opportunities that just weren't possible before. This has also increased competition, driven down costs, and improved the quality of services.

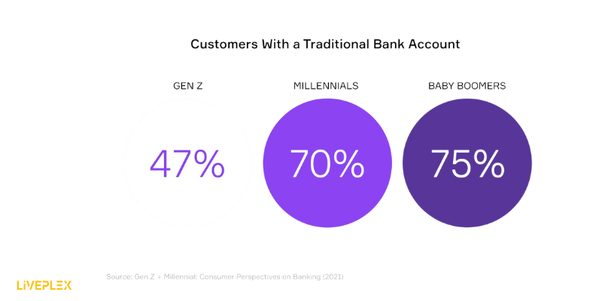

Global fintech funding reached $75.2B in 2022. Technology companies took the lead over financial institutions as the game changers in Fintech. A lesson was taught to the big banks about how to serve the younger demographic by digital banks and neobanks that embraced the motto, 'fewer branches, better apps'. Recent research indicates that Gen Z is much less likely to have a traditional bank account than Millennials or Baby Boomers.

Banks learned a valuable lesson from this. Even traditional institutions have been pushed to create smoother banking experiences through browsers and mobile applications since fintech turned the banking industry upside down in the past decade. It cost banks far too much to look the other way. As a result of being far more reactive to technological advancements and customer needs, banking executives are now focusing on (you guessed it) the metaverse. Is it really worth it? The short answer is yes.

Bloomberg estimates that the Metaverse market will reach $937 billion in 2030, up from $478.7 billion in 2020, at a CAGR of 41.6%.

So what is driving bankers to join the virtual bandwagon?

META-FI

The metaverse is not where we are going. Metaverses are already a part of our daily lives. Metaverses aren't new to those who have played Minecraft or other MMORPGs, so don't be surprised if you have.

A crypto bro's view differs from the metaverse we know by the paradigm to which they belong. In the bulk of games and In the world of Social 2.0, we use centralized platforms and a regulated financial system dominated by fiat currency. In Web 3.0, metaverses are built on the principles of privacy, data ownership, and decentralization.

Blockchains are synonymous with decentralization.

Blockchain provides a decentralized, transparent infrastructure that is at the core of Web 3.0. In this regard, it is ideally suited to handle the economies of these new virtual environments. Participants can move in and out of these economies seamlessly and access a wide array of compatible financial services rather than using in-game currencies and assets controlled by game developers.

DeFi (Decentralized Finance) stands as the logical next step in the development of MetaFi (Metaverse Finance). DeFi protocols and services can help power metaverse economies by securing the value of fungible and non-fungible assets.

For many banks, especially retail banks, De-Fi is becoming part of their everyday vocabulary. As central banks increase their efforts to develop Central Bank Digital Currencies (CBDC), we are just at the beginning of a revolution that is about to unfold.

With government-backed, regulated digital currencies, banks could enter the metaverse party in full swing and therefore run experiments that directly involve DeFi solutions.

As outlined in the paper “Lessons Learned from Decentralised Finance” by ING: “It is uncertain if DeFi protocols are actually in direct competition with banks at all [...] protocols for loanable funds are not directly acting as a full-fledged replacement for banks, because traditional banks are not intermediaries of loanable funds: rather, they provide financing through money creation”.

BUILDING VIRTUAL BRANCHES

Virtual branches are no longer just PR stunts for banks. Despite a lot of naysayers, the value of a branch that serves customers 24X7 and is location agnostic is a fair business ROI.

Even the most eloquent prophets of doom will understand the value of digital currencies as a value transfer mechanism. The inefficiencies of the current systems based on Web 2 lead to incompetent banking practices that perpetuate fraud, delays, and security breaches.

Would an MZ gen customer rather bank with a technically forward bank or a less efficient, technologically backward competitor? You reckon.

WITCE

As T-Mobile asks, What is in it for the Customer?

Is Gen Z the type of customer you imagine visiting bank branches?

Over the last decade, fintech, or financial technology, has become one of the hottest high-growth sectors as businesses embrace the idea of improving banking and other financial services by leveraging technologies and implementing a client-centric approach. This fascinating concept has revolutionized how people access financial services, which are now faster and more convenient than ever.

From online banking to peer-to-peer lending, the fintech industry has seen rapid expansion and innovation. These advances have made it easier for individuals and businesses to access financial services, creating opportunities that just weren't possible before. This has also increased competition, driven down costs, and improved the quality of services.

Global fintech funding reached $75.2B in 2022. Technology companies took the lead over financial institutions as the game changers in Fintech. A lesson was taught to the big banks about how to serve the younger demographic by digital banks and neobanks that embraced the motto, 'fewer branches, better apps'. Recent research indicates that Gen Z is much less likely to have a traditional bank account than Millennials or Baby Boomers.

Banks learned a valuable lesson from this. Even traditional institutions have been pushed to create smoother banking experiences through browsers and mobile applications since fintech turned the banking industry upside down in the past decade. It cost banks far too much to look the other way. As a result of being far more reactive to technological advancements and customer needs, banking executives are now focusing on (you guessed it) the metaverse. Is it really worth it? The short answer is yes.

Bloomberg estimates that the Metaverse market will reach $937 billion in 2030, up from $478.7 billion in 2020, at a CAGR of 41.6%.

So what is driving bankers to join the virtual bandwagon?

META-FI

The metaverse is not where we are going. Metaverses are already a part of our daily lives. Metaverses aren't new to those who have played Minecraft or other MMORPGs, so don't be surprised if you have.

A crypto bro's view differs from the metaverse we know by the paradigm to which they belong. In the bulk of games and In the world of Social 2.0, we use centralized platforms and a regulated financial system dominated by fiat currency. In Web 3.0, metaverses are built on the principles of privacy, data ownership, and decentralization.

Blockchains are synonymous with decentralization.

Blockchain provides a decentralized, transparent infrastructure that is at the core of Web 3.0. In this regard, it is ideally suited to handle the economies of these new virtual environments. Participants can move in and out of these economies seamlessly and access a wide array of compatible financial services rather than using in-game currencies and assets controlled by game developers.

DeFi (Decentralized Finance) stands as the logical next step in the development of MetaFi (Metaverse Finance). DeFi protocols and services can help power metaverse economies by securing the value of fungible and non-fungible assets.

For many banks, especially retail banks, De-Fi is becoming part of their everyday vocabulary. As central banks increase their efforts to develop Central Bank Digital Currencies (CBDC), we are just at the beginning of a revolution that is about to unfold.

With government-backed, regulated digital currencies, banks could enter the metaverse party in full swing and therefore run experiments that directly involve DeFi solutions.

As outlined in the paper “Lessons Learned from Decentralised Finance” by ING: “It is uncertain if DeFi protocols are actually in direct competition with banks at all [...] protocols for loanable funds are not directly acting as a full-fledged replacement for banks, because traditional banks are not intermediaries of loanable funds: rather, they provide financing through money creation”.

BUILDING VIRTUAL BRANCHES

Virtual branches are no longer just PR stunts for banks. Despite a lot of naysayers, the value of a branch that serves customers 24X7 and is location agnostic is a fair business ROI.

Even the most eloquent prophets of doom will understand the value of digital currencies as a value transfer mechanism. The inefficiencies of the current systems based on Web 2 lead to incompetent banking practices that perpetuate fraud, delays, and security breaches.

Would an MZ gen customer rather bank with a technically forward bank or a less efficient, technologically backward competitor? You reckon.

WITCE

As T-Mobile asks, What is in it for the Customer?

Is Gen Z the type of customer you imagine visiting bank branches?

When you think of Gen Z customers visiting bank branches, you might assume they would avoid them due to their lack of trust in traditional banks, reliance on digital services, and desire for further virtual developments. However, a Cornerstone Advisors survey reveals that young people still value bank branches for two reasons:

This preference is understandable given that customer service chatbots, which are commonly used in digital banking, often fail to satisfy customers.

A survey by GoMoxie found that 60% of banking customers aren't satisfied with chatbots and don't trust them. Similarly, a study by Phoenix Synergistics found that only 26% of consumers using AI-powered chatbots were very satisfied.

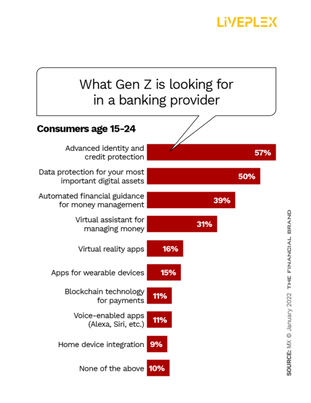

Gen Z's interest in virtual reality (VR) applications, virtual assistants, and automated guidance for money management demonstrates their desire for more personalized and "humanized" customer service.

As the Metaverse and Web 3.0 paradigms continue to shape our digital lives, banks must adapt to meet the evolving needs and expectations of their customers.

Ignoring this technological breakthrough would be a misguided decision, but thankfully, banks are already embracing the change.

The transformation of our relationship with money will create great opportunities for the financial sector, and banks should strive to be at the forefront of this innovation.

AI-LED AUTOMATION

According to research, AI has the potential to boost profitability for banks by 30% by 2025. But what does this mean for customers?

A survey conducted found that 73% of customers believe that AI can provide better financial advice than humans. And with the convenience and accessibility offered by virtual banking in the metaverse, customers can enjoy personalized financial solutions that cater to their specific needs and goals.

Banks are now able to get ahead of the curve and serve the new wave of customers in the industry by leveraging the power of Liveplex Web3 API stack.

Liveplex API technology also helps banks enhance their services by offering virtual financial advisors that can help customers make smart financial decisions in real-time. This technology can also help banks streamline their operations and improve efficiency by automating repetitive tasks, such as customer support and data entry.

With their ability to transform to Web3, banks can serve the new wave of customers and stay ahead of the competition.

For more, talk to us at hello@liveplex.io

- digital banking experiences are falling short of expectations, and

- they prefer dealing with humans for their financial affairs.

This preference is understandable given that customer service chatbots, which are commonly used in digital banking, often fail to satisfy customers.

A survey by GoMoxie found that 60% of banking customers aren't satisfied with chatbots and don't trust them. Similarly, a study by Phoenix Synergistics found that only 26% of consumers using AI-powered chatbots were very satisfied.

Gen Z's interest in virtual reality (VR) applications, virtual assistants, and automated guidance for money management demonstrates their desire for more personalized and "humanized" customer service.

As the Metaverse and Web 3.0 paradigms continue to shape our digital lives, banks must adapt to meet the evolving needs and expectations of their customers.

Ignoring this technological breakthrough would be a misguided decision, but thankfully, banks are already embracing the change.

The transformation of our relationship with money will create great opportunities for the financial sector, and banks should strive to be at the forefront of this innovation.

AI-LED AUTOMATION

According to research, AI has the potential to boost profitability for banks by 30% by 2025. But what does this mean for customers?

A survey conducted found that 73% of customers believe that AI can provide better financial advice than humans. And with the convenience and accessibility offered by virtual banking in the metaverse, customers can enjoy personalized financial solutions that cater to their specific needs and goals.

Banks are now able to get ahead of the curve and serve the new wave of customers in the industry by leveraging the power of Liveplex Web3 API stack.

Liveplex API technology also helps banks enhance their services by offering virtual financial advisors that can help customers make smart financial decisions in real-time. This technology can also help banks streamline their operations and improve efficiency by automating repetitive tasks, such as customer support and data entry.

With their ability to transform to Web3, banks can serve the new wave of customers and stay ahead of the competition.

For more, talk to us at hello@liveplex.io